Funding for the unconventional: Loans for manufactured, modular & mobile homes

When purchasing a home, it’s crucial to secure funding before entering into the transaction portion of the buying process. Typically, many homeowners go for a conventional loan, which is standard for most home types. But what about unconventional homes, such as a modular home, mobile home or even manufactured home?

Can you get this type of home with a conventional loan like a VA (Veterans Affairs) loan, FHA (Federal Housing Administration) loan or conventional loan? What about a personal property loan?

Here are three ways to secure funding for your unconventional home:

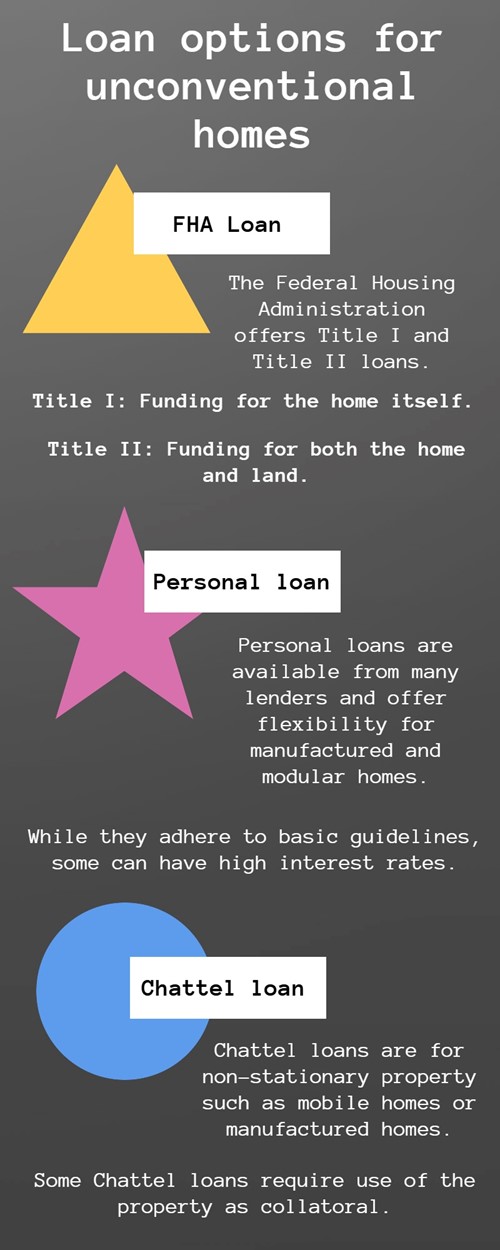

FHA loan

FHA loans are typically a popular option for those just starting their homebuying journey, first-time homebuyers and a slew of other potential homebuyers. Those searching for loans for mobile home options or manufactured home options may find peace of mind here.

FHA loans offer potential mobile homeowners either a Title I or Title II loan. Title I loans allow the prospective homeowner to simply borrow for the home, assuming all requirements are met. Homeowners who already have a mobile residence may be able to apply for this loan if they need to maintain or repair their home as well.

Title II loans help the buyer purchase the plot of land as well as the home being placed on it. These loans may have conventional term limits of 30 years, whereas Title I loans tend to max out at 20 years. Because of the stricter requirements of a Title II loan, most mobile homes won’t qualify due to being built before June 1976. Manufactured homes, however, will.

FHA loans used to secure these unconventional home types still require that home to be the borrower’s primary residence for approval.

Personal loan

Personal loans are a great way to circumvent numerous issues with conventional loans when it comes to mobile home loans, manufactured home loans and modular home loans. Personal loans are offered by a vast array of lenders, with some offering loans as high as $100,000.

Since personal loans are so flexible, they tend not to adhere to basic guidelines for unconventional homes. However, be wary of their interest rates. These loans can add up over time, so it’s best to review the terms, interest rates and monthly payments against your own financial plan.

Chattel loan

Chattel loans are typically offered for property that isn’t stationary, such as a mobile home or manufactured home. These loans typically require the borrower to enter into an agreement with the lender stating the residence or movable property are to be used as collateral in securing the loan.

While these may have more fees and risk associated with them, they are typically a good option for those in need of financing. For those with some financial restrictions, there are chattel loans with federal backing that may help you secure your home.

Be your home stationary or on the move, finding funding is one of the most important parts of the homebuying journey. Be sure to select the loan that’s best for you and your financial situation.

If you have questions about what type of financing, or even property type, to search for, give your agent a call. They’ll be able to help you move in the right direction for your new home.

About the Author

Rudden|Bobruska Team

Gary Rudden, Lisa Rudden, and Nick Bobruska

RUDDEN BOBRUSKA TEAM

What sets your team apart from other real estate teams?

There is no team out in the market that offers what we do. All of us are Realtors, but

we each have specialized roles, which make our team so unique!

After decades of living and selling real estate in the DMV, we have established

ourselves as one of the top real estate teams with our market expertise and

cutting-edge technology. Our savvy high-tech marketing is on every website

and social media source. We have a huge network with other top agents, which

helps to premarket homes and discover homes for buyers before they reach the

open market. Our services include professional in-house staging services, broker

expertise in negotiating and navigating contracts, and buyer representation in all

price ranges. Each client has different needs and we create a marketing plan based

on those needs.

Our most distinct feature is our in-house construction and renovation team. We

are literally a full-service, one-stop shop when selling or buying a home!

How does the in-house construction and renovation team work?

All work is managed and completed through our licensed and bonded construction

crew. No need to call outside contractors. We are like “HGTV,” but we just don’t

have a show! Whether it’s a small makeover or a major renovation, we do it all. Our

sellers love this aspect of our team because we make preparing your home for the

market so seamless. Our buyers love the advice and insight we can give for future

renovations and repairs.

Having a licensed Maryland Home Improvement contractor as part of our team

along with the knowledge, experience, commitment and services that we offer, truly

puts our team as a vanguard in the real estate industry.